Does Innovation Remain at Risk

Each year I look forward to getting the results of the Edelman Trust Barometer. The 2025 results should be published soon. Looking back to the 2024 Edelman Trust Barometer it revealed a paradox at the heart of society: while rapid innovation promises a new era of prosperity, it also poses significant risks. This duality is reshaping public perception and trust in technology and institutions.

Innovation has always been a double-edged sword. On one hand, it drives economic growth, improves quality of life, and solves complex problems. On the other hand, it can lead to job displacement, privacy concerns, and ethical dilemmas. The 2024 Edelman Trust Barometer highlighted that while people appreciate the benefits of innovation, they are increasingly wary of its potential downsides.

One of the key findings was the growing concern over data privacy. As technology advances, the amount of personal data collected and analyzed skyrocketed. This led to fears about data breaches, surveillance, and misuse of information.

Another significant issue was the impact of automation and artificial intelligence on employment. While these technologies increase efficiency and productivity, they also threaten to displace millions of jobs. The barometer indicated that people were anxious about their future job security and called for policies ensuring a fair transition for workers.

Moreover, the ethical implications of innovation are under scrutiny. From genetic engineering to AI decision-making, the potential for misuse and unintended consequences is a major concern. The public is urging for robust ethical guidelines and regulations to govern the development and deployment of new technologies.

The 2024 Edelman Trust Barometer underscored the need for a balanced approach to innovation. While embracing technological advancements, it indicated the criticality in addressing the associated risks and building trust through transparency, accountability, and ethical practices.

I’m interested to know how leaders in business and government have done since this barometer was released last year. Has trust in innovation made a comeback? What are you as a leader doing to advance innovation in an ethical manner?

- Are you managing innovation implementation effectively?

- Mismanaged innovations are as likely to ignite backlash as advancing progress. Explain the science and manage impacts aggressively

- Have you actively partnered with stakeholders?

- Business is most trusted to introduce innovation. Take the effort to partner with employees and government to manage the impact of innovation ethically.

- Are you engaging in active discussions with stakeholders about innovation implementation?

- When people are engaged in having control of how innovations affect their lives, they are more likely to embrace and advocate for the innovation, not resist them. Listen to concerns, openly

AI and the Complex Sale

Ever try selling something that doesn’t exist? Well, I suppose most software developers do that on a regular basis, but something BIG that takes years to design, build and deliver? I’ve been doing that for decades. From selling advanced weapons systems to governments to closing multi-year global technology implementations. It’s really complicated, hence the term Complex Sale.

They’re basically fancy words for “it’s going to take forever, and there are too many people in the room who think they’re in charge.” You’ve got committees, stakeholders, decision-makers—it’s like trying to agree on a group vacation, but worse because it involves money, egos, and PowerPoint slides.

Now, throw AI into the mix. What would take tons of work and years of intelligence gathering and suddenly, you’ve got insights, data, and predictions coming out of your ears.

The integration of artificial intelligence (AI) into the complex sales process is revolutionizing how businesses approach high-stakes transactions. By combining the computational power of AI with human expertise, sales professionals can navigate intricate sales cycles more effectively and deliver tailored solutions to meet diverse stakeholder needs. This fusion of technology and strategy is reshaping the landscape of complex sales.

AI’s Role in Chaos Control

AI is brilliant at sifting through the nonsense. Got a dozen people with different opinions? AI can sort out who actually matters in the decision-making process—spoiler alert: it’s not Geoff from Procurement. It analyzes emails, tracks behaviors, and somehow knows which stakeholder’s approval is critical. It’s like Sherlock Holmes but without the creepy violin.

And when it comes to objections, AI’s all over it. It’ll tell you things like, “They’re worried about price,” or “They think your delivery timeline is about as reliable as a politician’s promise.” Handy, right?

AI streamlines stakeholder management. By analyzing communication patterns and engagement levels, AI systems identify key decision-makers, anticipate objections, and tailor messaging to resonate with individual stakeholders. This data-driven approach ensures that every interaction is purposeful and aligned with the client’s needs

Relationship Building: AI Does the Admin

Let’s not pretend AI can charm its way through a room like a stand-up comedian. That’s still your job. But it’ll handle the boring stuff sellers hate—follow-ups, scheduling, tracking who said what and when. It’s like having an assistant who doesn’t complain or take weeks off to find themselves. Meanwhile, you can focus on the big stuff: being nice to people, listening to their concerns, and trying not to look too desperate.

Strategy, But Make It Smart

Here’s where AI really shows off. Predictive analytics—sounds fancy, doesn’t it? But basically, it’s AI looking at a load of numbers and going, “Yeah, they’re going to buy,” or “Forget it, they’ve already chosen someone else.” It’s brutally honest, which is refreshing in sales. No fluff, just facts.

And when it comes to negotiation, AI’s your secret weapon. It’ll tell you what worked in past deals, what’s likely to win them over, and even suggest a discount if that’s what it takes to close the deal. It’s like having a ringer on the softball team who slugs it out of the park every game but won’t take the credit.

Keeping It Human

The successful integration of AI in complex sales requires a balance between technological capabilities and human judgment. AI is clever, but it’s not human. It doesn’t do empathy, it doesn’t crack jokes, and it definitely doesn’t understand why you’re still trying to make “fax” happen in 2025. That’s where you come in. You’re the one who builds the relationships, makes people laugh, and convinces them that you’re the best option without actually saying, “Please, please pick me.”

The successful integration of AI in complex sales requires a balance between technological capabilities and human judgment. While AI provides valuable insights and efficiencies, it is ultimately the sales professional who interprets these insights and builds meaningful connections with clients. Emotional intelligence, creativity, and adaptability remain irreplaceable skills in navigating the nuances of human interaction.

The Future Is Here (and It’s a Bit Smug)

AI isn’t going anywhere and thank goodness for that. It’s saving us time, making us look smarter than we are, and helping us close deals that would otherwise take months. Just remember it’s a tool, not a miracle worker. The magic still happens when you combine its brilliance with your charm, wit, and uncanny ability to survive endless meetings.

So, embrace AI, but don’t let it get too cocky. After all, it’s just a machine. You’re the one

Sales teams must also remain vigilant about the ethical use of AI. Transparency in data usage, respect for client privacy, and avoiding biases in AI algorithms are critical to keeping trust and credibility.

Good sales teams are a tough crowd, they stick to what’s worked for them in the past. Bringing new tools and tech into the world of complex sales can be challenging, but AI is a true optimization enabler, apologies for the consultingese.

In the age of AI, the art and science of complex sales are converging like never before. By using the strengths of both, businesses can achieve new heights of efficiency, effectiveness, and customer satisfaction.

Chief Digital Officer (CDO) The What’s and Who’s

Digital transformations don’t happen all by themselves. Over the past decade as digitization of the enterprise has taken hold a new C-Level role has been appearing, the Chief Digital Officer.

The term “Chief Digital Officer” (CDO) started gaining traction in the early 2010s. According to Gartner, a leading research and advisory company, the CDO role was predicted to become a “hot executive title” by 2012, and they forecasted that by 2015, 25% of organizations would have a CDO. As is often the case, adoption predictions take longer to materialize than is thought. According to research from PwC, about 21% of large public firms now have a CDO. A little short of the 25% number predicted for 2015 but still a significant presence in the board room.

CDO’s play a crucial role in modern organizations, spearheading digital transformation efforts essential for businesses to remain competitive in today’s fast-paced, technology-driven world. The importance of the CDO lies in their ability to integrate digital technologies into every aspect of a company’s operations, driving enhanced efficiency, improving customer experiences, and unlocking new revenue streams.

What does a CDO do? CDO Role and Value

Driving Digital Transformation: At the heart of the CDO’s role is the responsibility to drive digital transformation across the organization. This involves not just implementing innovative technologies, but also rethinking and redesigning business processes to use digital capabilities fully. This transformation is essential for companies to stay relevant in an increasingly digital economy, where traditional business models are continually being disrupted by innovative digital solutions.

Enhancing Customer Experience: The CDO is tasked with improving the customer journey by using digital tools to provide seamless, personalized experiences. In a world where customer expectations are at an all-time high, businesses must deliver consistent, high-quality interactions across all digital touchpoints. The CDO ensures that the organization is equipped to meet these expectations by integrating customer data, leveraging artificial intelligence, and employing user-friendly digital interfaces.

Optimizing Operations: Digital transformation is not just about customer-facing changes; it also involves refining internal operations. The CDO works to streamline workflows, reduce inefficiencies, and improve decision-making through data analytics and automation. This can lead to significant cost savings and enhanced productivity, providing the company with a competitive edge.

Fostering Innovation: A critical aspect of the CDO’s role is to foster a culture of innovation within the organization. This involves encouraging experimentation with modern technologies, supporting digital initiatives, and promoting a mindset of continuous improvement. By driving innovation, the CDO helps the organization to stay ahead of technological trends and respond quickly to market changes.

Ensuring Cybersecurity: As businesses become more digitally integrated, the risk of cyber threats increases. The CDO handles implementing robust cybersecurity measures to protect the organization’s data and digital assets. This includes ensuring compliance with data protection regulations and fostering a culture of security awareness among employees.

What does a CDO look like? Typical Profile

Technological Smarts: A successful CDO must have a deep understanding of various digital technologies, including cloud computing, artificial intelligence, data analytics, and cybersecurity. This technical knowledge allows them to find and implement the right digital solutions for the organization.

Strategic Vision: The CDO should have a strong strategic vision to drive the digital agenda. This involves understanding the broader business context and aligning digital initiatives with the company’s overall goals. The ability to think long-term and anticipate future technological trends is crucial.

Leadership Skills: Effective leadership skills are essential for a CDO, as they must inspire and motivate the organization to embrace digital change. This includes leading cross-functional teams, managing resistance to change, and fostering a collaborative environment.

Business Acumen: The CDO needs a solid grasp of business fundamentals to ensure that digital initiatives deliver tangible business value. This includes understanding key performance indicators, financial metrics, and market dynamics.

Change Management: Driving digital transformation often involves significant organizational change. The CDO must be adept at managing this change, including communicating the benefits of digital initiatives, training employees, and ensuring a smooth transition.

Final Thoughts

The role of the Chief Digital Officer is pivotal in navigating the complexities of the digital age. By driving digital transformation, enhancing customer experiences, optimizing operations, fostering innovation, and ensuring cybersecurity, the CDO helps organizations to thrive in an ever-evolving technological landscape. What I find interesting is that in collaborating with my clients over the past decade since the inception of the CDO title I’ve never run into that role in any of my clients. It’s most often a project specific role that fills that space working with the C-Suite versus being a member of it. I’m looking forward to seeing the continued expansion of the role in all organizations over the next few years.

Digital Transformation:Erecting the House

The Challenge

In my last installment I discussed building the foundation for Digital Transformation. It’s time to erect that digital house on the strong foundation of business alignment that’s been poured and the clean-up of software debris completed. Adoption of new tools and processes always, and I mean always, represent the highest hurdles any enterprise must overcome to achieve digital transformation. Just a reminder that 38% of spend on these projects DO NOT mee their ROI objectives. So, 38 dollars or every 100 spent gets flushed into oblivion. In my experience that number is often higher but unrecorded.

Focus on Adoption

In my neighborhood a home built in the 1980’s has been undergoing a massive renovation, it’s been nearly 2 years since the whole process started. We were all very glad to see the changes, at first. To say that the neighbors are over-it is an understatement. Trucks everywhere blocking the street, a never-ending stream of contractors, noise and distraction have made all of us less than excited about the outcome, we just want it OVER! It’s the same phenomenon with digital transformation projects, employees see the value when the work begins but over time if the distraction of the change overshadows the intended outcome interest wanes and resistance builds. Consider that on any given day over 60% of employees are frustrated by new technology implementations. Successful digital transformation efforts understand this challenge and plan to reduce the risk.

Adoption Critical Success Factors

- Modernize Processes

- Redesign the business processes impacted by the change BEFORE implementing the digital tools. Never hope that the technology will change the processes by default.

- Work closely with key influencers in the process areas impacted to understand the work and build confidence that the technology improvements with make their lives easier and more productive.

- Memorialize the modernized processes on paper. Yes, on paper. Despite the notion that no one reads paper, employees want to see their new processes in front of them to understand, review and provide feedback.

- Design a Unified User Experience

- One password, one landing page, a unified experience that allows employees easy access to the new technology experience. There is no bigger mistake than to add passwords and landing pages to the already overloaded technology stack.

- Unified experiences that clearly mechanize the modernized processes give users the confidence needed to dive in and build competency. Forcing users to navigate new paths on top of old paths will make time to value increase significantly.

- Engage, Engage, Engage

- Introducing digitally transformed processes requires time and effort in engagement with the impacted employees. Build that time into the roll-out calendar. Shorting the initial adoption period is the biggest miss I see most often.

- Ensure senior leadership and process influencer involvement early and often.

- Focus on the WIIFMs (What’s In It For Me) value in every conversation. Users really don’t care much about the “bigger picture” value the digitization will produce; they focus on how it helps them do their job faster and easier. Unless everyone in the business owns stock in the company shareholder value is a poor WIIFM.

- Measure Adoption Religiously

- Observe usage regularly. Regularly depends on the process being performed some processes occur daily, others monthly or even less often, build a measurement scheme that takes these periods into account.

- Digital observation is only one way to measure adoption, it’s often the least reliable method. Digital monitoring will only provide a signal that adoption is weak, physical observation and measurement offers stronger data to assist users in adoption.

- Recognize Early Adopters

- Positive reinforcement of early adoption through highlighting success stories builds momentum for the changes implemented.

- Publicize stories about how customers are served more quickly and accurately than ever before or any other positive outcomes from early adopters.

Closing Thoughts

Digital transformation with embedded artificial intelligence is underway across the business community. Massive investment in digital technologies only produces the desired outcomes when these technologies become institutionalized as leading practice in your business. Be mindful of the positive steps you can take to reduce the risk of failure by planning carefully and executing flawlessly.

Digital Transformation: Real or Marketing Jargon?

Digital transformation—it sounds like the latest buzzword cooked up in a marketing lab, doesn’t it? But when you peel back the layers, you realize it’s far more substantive than flashy jargon. Let’s dig in.

A Little History

In my career I’ve been fortunate to grow and change at the pace of technology. In college I used a typewriter and carbon paper to author assignments and punch cards to program mainframes. So, I get the whole digital transformation thing deeply. But hasn’t it been going on since the mid-20th century? Understanding the contemporary version of digital transformation demands a look at history. The transition from analog to digital processes has been happening for decades. From the introduction of computers in the workplace to the rise of the internet, the shifts have been profound and continuous.

Take the Industrial Revolution, for instance. It was a period of tremendous change, with new machinery and technologies altering the way work was done. Similarly, the advent of computers in the mid-20th century marked the beginning of a new era. Businesses began to automate tasks that were previously manual, leading to increased efficiency and productivity.

Digital Transformation Evolution

The term “digital transformation” itself might feel new, but the concept is rooted in these historical shifts. Today, it refers to integrating digital technology into all areas of a business, fundamentally changing how you operate and deliver value to customers. This transformation is driven by the rapid advancement of technology and ever-increasing customer expectations.

In the 1990s, the rise of the internet brought about the first wave of contemporary digital transformation. Companies began to create websites, explore e-commerce, and digitize some of their operations. Some of us have scars to show from these early experiments where the website was the only digital part. Orders or inquiries may have been posted to the website but behind the scenes it was “rip and read” where we would rip the paper from the printer and read the internet result then manually execute the rest of the process. The early 2000s saw the rise of social media and smartphones, further pushing businesses to adapt. The current wave of digital transformation goes beyond mere digitization—it’s about rethinking and reimagining how businesses function in a digitally-driven world.

Not Just Marketing Hype

So, is digital transformation just marketing language? The evidence suggests otherwise. True digital transformation involves significant changes to business processes, culture, and customer experiences. It’s not about slapping a digital interface on an old process; it’s about fundamentally rethinking how to use technology to drive growth and efficiency.

Real-World Impact

Consider companies like Netflix and Amazon. Netflix started as a DVD rental service but transformed itself into a streaming giant by embracing digital technologies. Amazon, once an online bookstore, now dominates e-commerce and cloud computing thanks to its relentless focus on innovation and technology.

In manufacturing, digital transformation is manifesting as the Industrial Internet of Things (IIoT), where machines communicate with each other to optimize production, and digital twins allow virtual simulations of supply chain automation. In healthcare, digital transformation means better patient engagement through electronic health records and telemedicine.

Final Thoughts

Digital transformation isn’t just a shiny new term invented by marketers. It’s a continuing evolution that requires businesses to integrate digital technologies at their core. It’s about embracing the future while learning from the past. While the term may be relatively new, the concept is deeply rooted in the historical progression of technological innovation. So next time you hear the phrase, know that it’s more than just a buzzword—it represents today’s challenges and the future of business.

Over the next few weeks, I’ll be sharing tips and tricks to aid in the identification and adoption of digital technologies that drive transformations efforts.

Professional Certifications: Who Cares?

On a cold March morning many moons ago in Rockport, Massachusetts after completing our final open water certification dive the SCUBA instructor was pleased to say that we all had passed. He went on to remind us that all the little certification card meant was we could buy air at a dive shop, it didn’t mean we were divers, achieving that took the judgment that came with experience. My military jet instructor had a similar message when we got our wings, “those wings do not include judgment.” In both cases I described the certifications were only measures of a basic competency foundation opening the door to build ability.

Professional certifications are rampant in today’s fast-paced and competitive job market. They have become a popular way for individuals to demonstrate their skills and knowledge. However, the sheer number of certifications available has led me to question their value. Are all these professional certifications becoming meaningless?

The Rise of Professional Certifications

Professional certifications have long been a way for individuals to validate their expertise in a specific field. They are often seen as a mark of credibility and a way to stand out in a crowded job market. Over the past few decades, the number of available certifications has skyrocketed. From IT and project management to healthcare and finance, there seems to be a certification for almost every profession and skill set. In doing a search for the numbers of certificates available the only approximate number I could find was “thousands” actually many thousands.

Several factors have contributed to this growth:

- The rapid pace of technological advancement has created a demand for specialized skills. Certifications offer a way for professionals to keep up with these changes and show their proficiency.

- Increasing emphasis on lifelong learning and continuous professional development has led to a greater focus on getting new credentials.

- Online learning platforms have made it easier than ever to obtain certifications, further fueling their proliferation.

The Dilution of Value

While the increase in certifications offers more opportunities for professional development, it also raises concerns about their value. One of the main issues is the lack of standardization. With so many certifying bodies and programs, the quality and rigor of certifications can vary widely. This inconsistency makes it difficult for employers to assess the true value of a certification and for professionals to know which credentials are worth pursuing.

Another concern is the commercialization of certifications. Many organizations have recognized the lucrative potential of offering certification programs and have flooded the market with new credentials. This has led to a situation where almost anyone can obtain a certification, often with minimal effort or investment. As a result, the prestige and significance of certifications have diminished, and they are no longer seen as a reliable indicator of expertise.

The Impact on Professionals and Employers

The proliferation of certifications has created a challenging landscape for both professionals and employers. For professionals, the pressure to obtain multiple certifications can be overwhelming and costly. It can also lead to a focus on accumulating credentials rather than developing deep, meaningful expertise. This credentialism can create a false sense of competence and undermine the importance of practical experience and critical thinking skills.

For employers, the abundance of certifications complicates the hiring process. With so many credentials to choose from, it can be difficult to determine which ones are truly valuable and relevant to the job. This can lead to a reliance on certifications as a shortcut for assessing candidates, rather than a comprehensive evaluation of their skills and experience.

Invest in Certifications Wisely

Despite these challenges, certifications can still hold value if approached thoughtfully.

- Professionals:

- Focus on obtaining certifications that are recognized and respected within your industry.

- Prioritize continuous learning and practical experience over simply accumulating credentials.

- Employers:

- Take a holistic approach to evaluating candidates, considering certifications as one of many factors in the hiring process.

Self Service Off the Rails

Yesterday I spent 2 hours climbing in my attic, crawling under sinks and behind toilets in service to my insurance company. Seriously? Apparently to save money my outrageously expensive insurance company decided that I should conduct my own self-inspection using a really shitty app providing them access to the perils of my toilet connections.

This is a version of self-service that is off the rails, out of bounds and an affront to the value I get from any insurance company. By the way, in over 4 decades of paying tens of thousands of dollars for homeowners’ insurance I have never filed a single claim, not one. The reward, go ahead and spend your time doing our job.

If this sounds like a rant, it’s because I’m angry and disappointed in how far businesses have taken self-service. Apparently, today’s business just provides a “thing” whether it’s a product or service they take no responsibility for actually serving their customers. Your app not working, try finding a human to help. Car breaks down and need a tow, you better have signal coverage and the app installed. I think you get the drift here. This all started when we began pumping our own fuel at service stations and has gotten wildly out of control.

I take some responsibility for these practices as a customer experience expert advising clients on how to both be efficient and customer focused simultaneously. Self-service is a tool in the bag but shouldn’t be the only tool.

I’m quite sick of having to download an app for everything in my life. From coffee shops to banking to utilities the world has gone application crazy. Data is the true commodity that every business is selling today, the insatiable appetite for more data has destroyed customer service. The thirst for personalizing every offer through the endless number of apps. On average we have about 35-40 apps installed on our smartphones. That means we carry between 35 and 40 cards in our wallet to conduct daily life. Imagine the size of your wallet. But since these cards are virtual and have no physical footprint, we don’t care, it’s just another icon on a screen.

I hope my point is clear, if a business wants to differentiate itself in a wildly competitive market take a stand and care for your customers with real-time support for your product and service. Self-service or Level Zero support is important for the mundane like password resets but don’t put customers into an endless loop of time wasting to access Level 1,2, and 3 support. Your customer’s time is just as valuable as your time, even more valuable as they pay your bills. Understand that one simple concept and you can differentiate.

There’s an App for That…

How many apps, a.k.a applications, do you have on your device? I bet you have no idea how many apps you carry around. I certainly don’t but I do know how many I use regularly, and the answer is about 5 or 6.

So, I did a little research using Bing Copilot and the findings were staggering.

The typical number of mobile apps that a smartphone user carry can vary, but here are some relevant statistics:

Monthly App Usage:

On average, a smartphone user accesses 30 mobile apps in a month, which translates to roughly 10 apps every day.

App Store Availability:

Apple’s App Store boasts a staggering 1.96 million apps available for downloads.

Google Playstore, catering to Android users, offers an even larger selection with 2.87 million apps.

Frequency of App Usage:

Approximately 49% of people open an app more than 11 times a day.

Interestingly, 21% of individuals between the ages of 23 and 38 open an app more than 50 times in a single day.

These numbers represent just how dependent humans are on technology these days. There are nearly 3 million apps available to download. What do all these little pieces of software do, exactly?

As I’m having fun playing with app numbers let’s do a little more math.

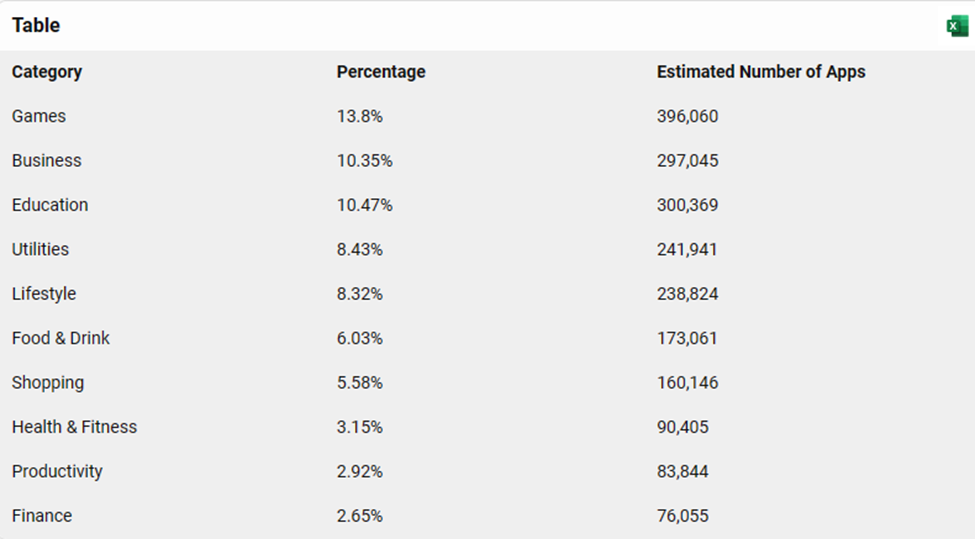

Here’s a table that breaks down the estimated number of apps per category based on the total size of available apps at 2.87 million in the Google Play Store:

These figures are calculated using the percentages provided for each category and the total number of apps in the Google Play Store. Keep in mind that these numbers are estimates and can change as the app market evolves.

Not to be hyperbolic but this is CRAZY!!! 396,000 games, really? Nearly 300,000 business apps? Holy overload!

More fun with math, I asked Copilot to calculate the number of apps per person on Earth. Using the total number of app downloads and the global smartphone user count. As of 2024, there are 4.88 billion smartphone users worldwide1, and the total number of app downloads has reached 257 billion2.

Using these figures, we can estimate the average number of apps downloaded per smartphone user:

So, on average, each smartphone user has downloaded about 53 apps.

These numbers indicate a serious addiction to apps. So, if we take it from the top of this discussion where we saw that the average user accesses 30 apps per month with the potential to download 53 apps per month what is the point of all these technologies?

What’s the Value of Each App

I ask this question only to highlight the business issue of value. Where does the value lie for investors? How many new apps can be supported by the user community? There is no data available for the length of time that an app is viable in the marketplace, it may be years for some and weeks for others.

The average value of a mobile app can be determined by various factors, including its revenue, user base, and market demand. A common valuation method is to calculate the app’s value based on its average monthly revenue multiplied by a specified number of months. For instance, if an app generates $500 a month, it might be valued at 6 months’ worth of revenue, or $3,0001.

For apps that are post-revenue (already generating some income), a simple valuation formula could be:

Valuation=(CLV−CAC)×number of users

Where:

- CLV (Customer Lifetime Value) is the total net margin earned per user over their lifetime.

- CAC (Cost of Acquisition) is the cost to acquire a user.

This formula assumes the valuation is equal to the sum of all users’ average customer lifetime value minus their cost of acquisition2.

However, it’s important to note that app valuations can vary widely and are ultimately determined by what a buyer is willing to pay for it. Factors such as growth prospects, niche, and consistent revenue can influence the multiple used to calculate the final valuation. For example, an app generating $100,000 in net cash flow per year might be valued between $200,000 and $300,000, using a multiple of 2x to 3x3.

The cost of developing an app can also provide insight into its value. On average, building a mobile app can range from $100,000 to $500,000, with some feature-rich apps costing more than half a million dollars4

Be Diligent

Whether you’re a burgeoning founder of a new application offering or an investor looking for the next killer app you must be diligent.

- Research currently available apps in your category of interest.

- Determine the “white space” available, there isn’t much.

- Identify the functions users must have and those that will differentiate your offering.

- Develop an MVP (minimal viable product) quickly

- Test, test, test. Test the market, test the technology, test your resolve.

There will always be a market for the next “cool” app. Just be diligent before you spend mom and dad’s retirement fund.

A Twisted Pair: Growth & Risk Mitigation

We are surrounded by opportunities. Each opportunity brings with it inherent risks. Just looking around at everything we do every day there is risk around every corner. From crossing the street to grilling on a barbeque, risk is all around us. Navigating risk is the foundation of growth, both in life and in business.

Whether you’re a startup founder or a seasoned business leader, navigating risks effectively will significantly impact your company’s growth trajectory. How we manage that risk makes all the difference. Examples of typical risks include both internal and external factors. Common internal risks include operational inefficiencies, talent management, inadequate financial controls, or poor strategic planning. External risks range from economic downturns to regulatory changes or supply chain disruptions. These are only a few of the risks that could be encountered on a regular basis. What a mess!

I’ve found in my experience that an abundance of the potential risks can be determined well in advance of a crisis occurring if we keep our eyes open and ears to the ground. Situation awareness is crucial for risk management to be an ally. Seeing the whole picture of the business environment in context to your own endeavors will allow you to see well in advance of serious risks so that mitigation actions can be taken, and growth scenarios built.

Thinking about risk management is everyone’s responsibility. I’ve highlighted a few things to consider in helping ensure growth and risk can work in synergy.

1. Identify and Assess Potential Risks

Before mitigating risk, you must understand what you’re up against. Conduct a comprehensive risk assessment by considering both internal and external factors. Execute the identification process deliberately as part of your planning cycle. Log the risks, rank them for severity and probability of occurrence.

2. Plan for Potential Scenarios

Anticipate potential risks by creating various scenarios. What if demand suddenly drops? What if a key supplier goes out of business? Scenario planning helps you prepare for the unexpected. Develop contingency plans for each scenario, ensuring that your business can adapt swiftly when needed. This is where the latest in Artificial Intelligence (AI) can make a huge difference. The latest AI technology allows for rapid scenario analysis.

3. Spread the Risk

Diversification isn’t just for investment portfolios; it applies to business risk as well. Relying too heavily on a single product, market, or customer can be dangerous. Diversify revenue streams, expand into new markets, and build a resilient customer base. By spreading the risk, you hedge against the impact of any single risk event.

4. Build Resilient Operations

Build operational resilience by investing in robust processes, redundant systems, and disaster recovery plans. Regularly test these mechanisms to ensure they function seamlessly during crises. A resilient business can weather storms without compromising customer satisfaction or core operations. Our recent experience with the global pandemic puts a fine point on resiliency. During that period, I saw some of my clients scramble to implement remote communications processes for typically desk bound employees or rapidly invest in innovative methods to manage their disrupted supply chains. Build to weather any storm.

5. Watch the Data

Leverage data analytics to identify patterns and predict potential risks. Monitor key performance indicators (KPIs) and track deviations. Early detection allows you to take corrective actions promptly. Whether it’s detecting fraud or optimizing supply chain logistics, data-driven insights enhance risk management.

6. Embrace Change

Risk management isn’t static; it’s an ongoing process. Stay informed about industry trends, regulatory changes, and emerging risks. Maintain a high level of situation awareness. Adapt your strategies accordingly. A growth-oriented business embraces change and learns from both successes and failures.

7. Lead with Commitment

Risk management starts at the top. Leaders must champion a risk-aware culture. Encourage employees to report risks without fear of reprisal. When everyone understands their role in mitigating risk, the entire organization becomes more resilient.

The twisted pair of business growth and risk management go hand in hand. By proactively identifying, assessing, and mitigating risks, you pave the way for sustainable expansion. Remember that risk isn’t the enemy—it’s an opportunity to innovate, adapt, and thrive.

About The Change Dude

Outside the blogoshpere I’m Bob Caruso, a professional change artist/Managing Partner at Orchid Black.

Most people don’t particulary like when things around them are constantly challenging their ability to walk in a straight line. I, on the other hand, love it when the status quo was 10 minutes ago. Over the past 30 years I’ve been assisting people and organizations reinvent, reinvigorate and renew themselves. It’s a blast!

On a more professional note…I bring 35 years experience in implementing large scale change as both an executive and professional consultant. Through that time I’ve carried business cards for some formidable firms including Rockwell, Price Waterhouse, Deloitte and J.D. Power and Associates. For more about my professional history visit http://www.linkedin.com/in/bobcaruso.

Visit me here to get the opinions, advice and connections you may be looking for when the string in your life gets a bit kinky.

-

Recent

- Does Innovation Remain at Risk

- AI and the Complex Sale

- The Power Play of ‘Let Me Finish’: Strategies to Foster Open Dialogue

- Navigating Life’s Unkown Journey

- Chief Digital Officer (CDO) The What’s and Who’s

- Digital Transformation:Erecting the House

- Digital Transformation: Real or Marketing Jargon?

- The Price is Right: Cracking the Code of Productivity

- Disaster Communications

- Professional Certifications: Who Cares?

- The Age of the Itinerant Professional

- Wisdom versus Knowledge in the Age of AI

-

Links

-

Archives

- January 2025 (2)

- December 2024 (1)

- November 2024 (3)

- October 2024 (3)

- September 2024 (3)

- August 2024 (4)

- July 2024 (3)

- June 2024 (2)

- May 2024 (5)

- April 2024 (4)

- March 2024 (4)

- February 2024 (2)

-

Categories

-

RSS

Entries RSS

Comments RSS